The Mortgage Bankers Association has long supported modernizing the credit reporting requirements that govern the mortgage origination process. I want to reaffirm that position and explain why the evidence today — and responsible policy design — point clearly in one direction: we can safely remove the universal tri-merge mandate for loans sold to Fannie Mae and Freddie Mac.

What the research shows

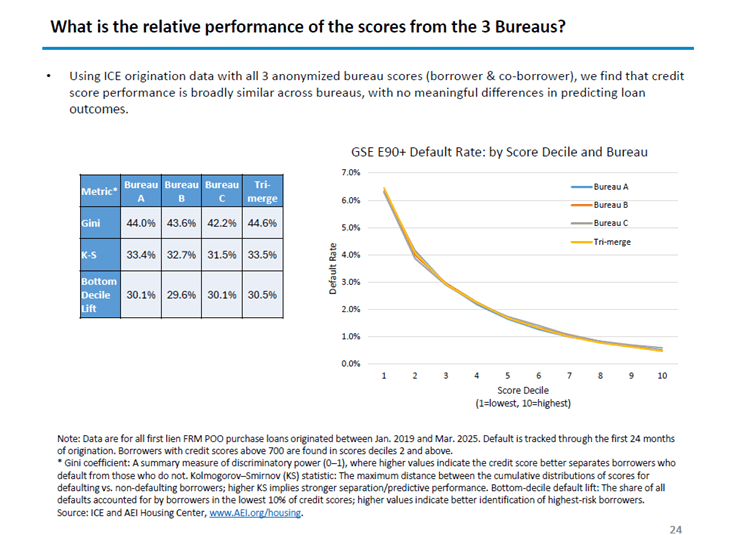

A compelling study from the American Enterprise Institute provides important empirical grounding for this discussion. The research demonstrates that a single credit score carries essentially the same predictive power as the tri-merge approach — the longstanding practice of pulling reports from all three major bureaus and using the middle score.

In other words, when used properly, one score derived from a single report can tell lenders what they need to know.

That qualifier — when used properly — is critical, and I’ll come back to it in a moment.

The case for reform

The tri-merge requirement adds cost and complexity to the origination process without a commensurate benefit in credit risk assessment — at least for well-qualified borrowers with strong credit histories. Reducing the reporting burden can lower origination costs, simplify the process for consumers, and streamline underwriting workflows. These are meaningful gains that the industry and borrowers alike stand to benefit from.

Where MBA draws the line — and why it matters

The AEI research is clear on an important condition: the predictive equivalence of a single score holds only when lenders are not gaming the system. The risk in a single-score environment is that some lenders might pull multiple individual scores and select the highest — effectively shopping for the most favorable result rather than getting an accurate picture of a borrower’s creditworthiness. That practice could undermine the very integrity the reform is meant to preserve.

MBA’s position

MBA strongly supports implementing clear business rules that prohibit lenders or borrowers from gaming the system to provide only the top score and accompanying report. For example, lenders should be prohibited from pulling multiple reports/scores and cherry-picking the highest – if you pull three reports/scores, you must submit all three. Lenders could also be required to select a specific bureau—who would compete for that business—for the initial credit pull.

Any move to a single score and report framework must be paired with enforceable guardrails that prevent manipulation. Without them, we risk trading one inefficiency for a new form of gaming that ultimately harms consumers and market integrity.

A targeted reform, not a blanket one

MBA’s support for a single score and report approach is also appropriately scoped. We believe this reform should apply to loans for borrowers with strong credit profiles to provide an extra “safety net” while beginning necessary credit score competition. For borrowers with lower scores — where the nuances across bureau reports may carry greater weight — the current tri-merge framework may still offer some useful functions. Our support is not a call for wholesale elimination of the tri-merge across all borrower categories, but a targeted, evidence-based modernization that will safely introduce competition to the credit report market and inform future decision-making.

And, lenders would always have the option to obtain a tri-merge if they choose.

The bottom line

The AEI research reinforces what many in this industry have long believed: the tri-merge requirement, as applied to well-qualified borrowers, is a relic that adds cost without adding meaningful insight. The GSEs’ conservator, FHFA, determined more than three years ago that a tri-merge was not necessary. MBA supports reform — but importantly, reform done right. That means a single report and score, and strict anti-gaming business rules.

Insulated from competition by the tri-merge mandate, the credit bureaus and score provider have exploited their monopoly pricing power and raised prices aggressively over the past five years. It’s time for reform. We look forward to continued engagement with policymakers, regulators, and industry stakeholders to ensure that changes to the credit reporting framework are implemented thoughtfully, with safeguards that protect taxpayers, lenders, and the borrowers they serve.